Practical Considerations in Legacy Planning

For many families, estate planning is viewed mostly as a tax discussion. That is certainly part of it, but once wealth reaches a certain level, the conversation becomes much broader.

Beginning in 2026, the federal estate tax exemption is $15 million per person, or $30 million for a married couple with proper planning. Importantly, the exemption is now considered permanent law rather than subject to a scheduled “sunset” provision. While future Congresses can always change tax law, the planning environment is now far less uncertain than it was over the last several years, when many families worried about exemptions suddenly being cut in half.

For families below these exemption levels, estate taxes may not ultimately be the primary concern. However, this is often exactly the point where trust planning starts to become much more important.

This is not necessarily because of taxes. In fact, many families in this range may never pay federal estate tax at all. The bigger issue becomes structure, protection, control, and continuity across generations.

For example, a family may want assets protected from future lawsuits, divorces, creditors, or simply poor decision-making by future beneficiaries. Others may want wealth to remain inside the family bloodline over multiple generations instead of passing outright to children and then becoming fragmented over time. In many cases, the goal is not simply to maximize wealth, but rather to organize it intelligently.

This is where trusts begin to play a much larger role.

A properly designed trust can provide meaningful benefits to a beneficiary without requiring that assets be distributed outright. A beneficiary can receive cash flow, investment support, help with education, housing, healthcare, or other needs, while the underlying trust assets remain protected and professionally managed.

This structure can be very important. If assets are distributed outright, they can potentially be exhausted irresponsibly, attached through lawsuits, divided in a divorce, or even pressured away through coercion by others. A beneficiary under financial stress, emotional pressure, addiction issues, or legal judgment may make decisions very differently than originally intended by the family members creating the wealth.

In contrast, assets held inside a properly structured trust are often far better protected. The beneficiary can still benefit from the trust, but without necessarily having unrestricted access to the principal. This creates a balance between support and protection.

In some cases, trusts are designed to continue generation after generation, creating what is often referred to as a “legacy trust.” The purpose is not to create control from the grave, but rather to preserve flexibility, stability, and family opportunity over long periods of time.

The practical reality is that wealth without structure can create unintended problems. A good estate plan is not simply a legal document package. It is a framework designed to protect assets, simplify administration, and create long-term clarity for the family.

Funding the Trust

For most families, the foundation of an estate plan is a revocable trust paired with a “pour-over” will. This is the standard structure for many well-designed estate plans because it provides organization, flexibility, continuity, and privacy.

A revocable trust is exactly what it sounds like… revocable. During your lifetime, you remain in control. You can amend the trust, change beneficiaries, replace trustees, move assets in or out, or revoke the trust entirely. From a practical standpoint, assets inside the trust are still effectively your assets while you are living.

Typically, accounts and property are retitled into the name of the trust during life. For example, investment accounts, real estate, and other assets may be owned by:

“The John and Jane Sample Revocable Trust.”

The pour-over will acts as a safety net. If an asset is accidentally left outside of the trust, the will directs that the asset “pour over” into the trust at death. In this way, the trust becomes the central controlling document.

One major advantage of the revocable trust structure is continuity. If incapacity occurs, the successor trustee can step in and continue managing assets without the disruption of court proceedings or guardianship actions. At death, assets inside the trust also generally avoid probate, which can simplify administration, preserve privacy, and improve efficiency for the family.

Married couples may either use one joint revocable trust or separate trusts for each spouse. A joint trust is administratively simpler and works well in many situations. However, separate trusts can sometimes provide additional flexibility for income tax planning. For example, if one spouse is in materially worse health, highly appreciated securities may intentionally be placed in that spouse’s trust in order to maximize the step-up in tax basis at death, while loss positions or less appreciated assets may remain in the healthier spouse’s trust. For families with large low-basis investment positions, this type of planning can materially reduce future capital gains taxes.

For many families, the revocable trust is the starting point. From there, planning can become more advanced depending on the goals.

Funding Trusts During Lifetime

In some cases, trusts are funded during lifetime rather than waiting until death. This is especially common when families want to begin moving assets to children or future generations in a gradual and organized way.

One of the simplest strategies involves annual exclusion gifting.

Each person can gift up to $19,000 per year to any individual without using any portion of the lifetime estate and gift tax exclusion and without paying gift tax. For a married couple, this amount effectively doubles to $38,000 per beneficiary through “gift splitting.”

Over long periods of time, especially when combined with investment growth, these transfers can become very meaningful. This becomes particularly important for families whose assets may eventually exceed the federal estate tax exemption amounts. Assets above the exemption are generally subject to federal estate tax at a 40% rate. So, every $1 million above the exemption may create approximately $400,000 of federal estate tax.

As a result, even gradual lifetime gifting programs can materially reduce future estate taxes, particularly when appreciation on the gifted assets also occurs outside of the taxable estate.

Importantly, annual exclusion gifts do not need to be made outright to beneficiaries. In many cases, gifts are instead made into trusts for the benefit of children or grandchildren. This allows the family to move assets outside the estate while still maintaining structure and protection around how the funds are ultimately used.

In order for gifts to a trust to qualify for the annual exclusion, the trust is often drafted with limited temporary withdrawal rights for the beneficiaries, commonly referred to as “Crummey powers.” In practice, these provisions are usually administrative in nature and are designed to preserve the tax qualification of the annual gifts.

Some families choose to use a portion of their lifetime estate and gift tax exclusion early by making larger transfers into irrevocable trusts during life. The logic is straightforward… if assets are expected to appreciate significantly over time, moving them out of the estate earlier can allow all future growth to occur outside the taxable estate.

There are more advanced “leveraged” planning strategies designed to move greater economic value into trusts relative to the amount of gift exclusion used. Depending on the circumstances, this may involve valuation discounts, sales to intentionally defective grantor trusts, GRATs, QPRTs, family partnerships, life insurance structures, or other techniques. The details become highly technical, but the general idea is to maximize the long-term value shifted to future generations while minimizing the amount of exemption consumed.

Of course, gifting strategies should be approached carefully. Families must balance long-term planning goals with maintaining sufficient assets and flexibility for their own future needs.

Trust Distributions

One of the most important parts of trust design is determining how distributions should work for beneficiaries.

Older trusts were often written to distribute only “income” to beneficiaries. Years ago, this made more sense because many investment portfolios were designed around dividend-paying stocks and bonds. Trust beneficiaries would receive the interest and dividends generated by the investments while the underlying principal remained protected for future generations.

Today, investment portfolios work very differently. Many high-quality investments generate little income and instead grow through capital appreciation. As a result, older “income only” trust language can sometimes create unintended limitations. Modern trusts therefore tend to give trustees much broader flexibility.

The most common standard allows distributions of both income and principal for a beneficiary’s “health, education, maintenance, and support.” These are the usual words that give the trustee flexibility.

“Health” may include medical care, insurance, long-term care, or mental health treatment. “Education” could include college, graduate school, trade school, tutoring, or professional training. “Maintenance” and “support” are broader lifestyle standards, allowing the trustee to help maintain a reasonable standard of living consistent with the family’s intentions.

This flexibility is important because beneficiaries may have very different needs over time. One beneficiary may need help purchasing a home or navigating a difficult financial period, while another may be financially independent and require little support.

At the same time, many families still want some guidance around distributions rather than leaving decisions completely open-ended. As a result, trusts often include non-binding language expressing the family’s intent. For example, a trust may suggest that trustees attempt to limit long-term distributions to approximately 4% annually, similar to a prudent endowment spending policy. This type of guidance can help preserve the long-term purchasing power of the trust while still providing meaningful support to beneficiaries.

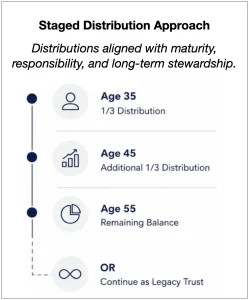

Some trusts also provide for distributions of principal at specific ages. For example, one-third of the trust may distribute at age 35, another third at age 45, and the balance at age 55. For moderate-sized trusts, staged distributions may make sense because they gradually transition responsibility to the beneficiary over time.

For larger trusts, serious consideration is often given to maintaining assets inside a long-term “legacy trust” structure rather than distributing principal outright. Under a legacy trust, assets can remain in trust generation after generation while beneficiaries continue receiving support and benefits under the trust terms.

Historically, many states limited how long trusts could continue through what was known as the “Rule Against Perpetuities.” Over time, many states significantly modified or eliminated these restrictions, making very long-term or perpetual trust structures possible. As a result, modern legacy trust planning has become much more common.

A very important practical point is that trusts for children are often divided into separate “trust shares” after the death of the parents. In other words, each child’s portion is usually held in a separate trust rather than keeping all siblings inside one combined structure. This separation can be extremely important. Different beneficiaries often have different spending patterns, financial needs, investment preferences, family situations, and personalities. Separate trust shares help avoid situations where siblings feel they are subsidizing one another or disagreeing over distributions, investment decisions, or trustee actions. In practice, separating the trusts often greatly simplifies administration and helps reduce family tension over time.

Tax on dividends and income at the trust level can often be higher than the beneficiary’s individual tax rate. A trustee should monitor this and potentially shift taxable income to the beneficiary by distributing the income.

The Role of Trustee

The trustee ultimately controls how the trust functions in the real world.

During the period when a trust is revocable, the person creating the trust is typically both the trustee and beneficiary. In other words, nothing really changes from a practical standpoint during lifetime because the creator of the trust still controls and benefits from the assets. However, an additional co-trustee can be added if desired, or a successor trustee can step in later if health declines, incapacity occurs, or assistance is needed with administration and investment management.

Once the trust becomes irrevocable, the trustee structure becomes much more important. The trustee is responsible for investment oversight, recordkeeping, tax reporting, administration, distributions to beneficiaries, and following the terms of the trust document. In many ways, the trustee acts as the “manager” of the trust structure over time.

Historically, trusts were often managed almost entirely by banks and trust companies. While professional trustees can provide stability and technical expertise, older bank trust arrangements developed a somewhat negative reputation in some families. Complaints often included inflexibility, bureaucratic administration, slow decision-making, high fees, and trustees who did not truly understand the personalities and dynamics within the family. As a result, many modern estate plans try to incorporate family involvement where practical.

In many cases, it is beneficial to have a trusted family member serve as trustee or co-trustee because they better understand the intricacies of the family, the personalities of beneficiaries, family values, spending habits, and the intent behind the planning. A family trustee may also be more flexible and practical when unique situations arise.

At the same time, there are important reasons to include an independent trustee as part of the structure. An independent trustee is typically someone without a beneficial interest in the trust, such as a trusted advisor, attorney, CPA, professional fiduciary, or trust company. Independent trustees often bring stronger technical knowledge regarding trust administration, taxation, investment oversight, and fiduciary responsibilities.

Independent trustees can provide an added layer of creditor and asset protection. If a beneficiary has unrestricted authority over distributions to themselves, the trust assets may become more vulnerable to creditors, divorces, or legal claims. By requiring an independent trustee to participate in certain distribution decisions, the protective nature of the trust is often strengthened.

As a result, many modern trusts use a blended approach. For example, a beneficiary may serve as trustee of their own trust for administrative convenience and family familiarity, while an independent trustee is required to approve broader discretionary distributions. This structure can create a balance between flexibility, practical family understanding, and long-term protection.

Another important feature is the ability to name successor trustees. A trust may continue for decades, potentially over multiple generations. Naming successor trustees allows continuity if the original trustee resigns, becomes incapacitated, or passes away. Many trusts also allow beneficiaries or family members to replace trustees under certain conditions, creating additional flexibility over time.

No single trustee structure is perfect for every family. The goal is usually to create a system that combines technical competence, good judgment, family understanding, continuity, and protection.

Other Trust Considerations

Modern trust planning often includes provisions designed to create flexibility over long periods of time, since family situations, tax laws, and financial circumstances can change dramatically across generations.

One important tool is a “power of appointment,” which allows a beneficiary to redirect where trust assets ultimately pass at their death. This prevents the trust from being permanently locked into decisions made decades earlier. There are generally two types:

- General Power of Appointment – Allows assets to be appointed broadly, including potentially to the beneficiary, their estate, or creditors. This level of control can create estate tax inclusion.

- Limited (or Special) Power of Appointment – Allows assets to be redirected only among a defined class of beneficiaries, such as descendants or charities. This is more common in legacy trust planning because it preserves flexibility while maintaining asset protection and estate tax benefits.

For example, a child may later decide that one grandchild has greater needs than another. A limited power of appointment allows adjustments without rewriting the trust structure.

Another important role in many modern trusts is the “trust protector,” often an attorney or independent advisor who may have authority to replace trustees, address tax law changes, or modify administrative provisions over time. This adds another layer of flexibility for trusts expected to continue over multiple generations.

It is often desirable to include “grantor trust” language in a trust document. Under this structure, the creator of the trust continues paying the income taxes generated by trust assets, even though the assets may be outside of their taxable estate. While this may initially sound unfavorable, it effectively allows additional tax-free wealth transfers into the trust because the trust assets continue compounding without reduction for taxes. Grantor trust status can also create planning flexibility because certain transactions between the grantor and the trust are ignored for income tax purposes.

Families with larger estates should consider generation-skipping transfer (“GST”) tax planning. Proper allocation of GST exemption can allow assets to remain inside long-term multi-generational trusts without being subject to estate tax again at each generation.

Families should periodically review beneficiary designations on retirement accounts, insurance policies, and transfer-on-death registrations to ensure they coordinate properly with the trust structure.

The best estate plans are usually not the most complicated. They are the plans that create flexibility, clarity, protection, and long-term practicality for the family members involved.