First Half Of 2026: Market Outlook, Oil Disruptions, & Economic Resilience

The credit crisis in 2008/2009 brought to the surface “the unknown unknown.” While conflict in the Middle East is not an unknown, the initiation (or at least the timing) of the war with Iran was somewhat unexpected. As a result, the investment markets are rockier than they have been, underscoring the value of disciplined investment management, but investors still see big opportunity in AI and are mostly “bullish” on the economy. Despite macroeconomic headwinds, the underlying strength in technology sectors is providing a buffer against broader market panic.

The oil supply is under pressure, which will likely prove to be a shorter-term issue. All countries involved need oil to be transported freely and safely. However, conflicting headlines day-to-day are an excuse for investors to question stock prices. We can see this in daily price movements. Since 2022 (with early 2025 being the brief exception), the tendency was up. Investors felt good. The recent market feeling is the opposite, with a downward tendency even if there is a good headline. Thankfully, the magnitude has been muted relative to other world events, such as Russia’s invasion of Ukraine in 2022.

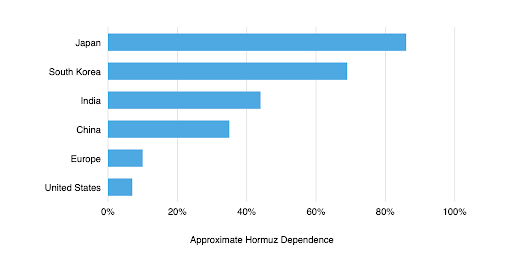

Headlines are sensational: “The biggest energy crisis since the 1970s.” This is unlikely for the U.S., because only a small portion of oil imports come through Hormuz. In contrast, Japan gets 90% of its oil shipped through the Strait. In the overall global economy, the oil disruption is just that… a disruption, not a major crisis like in the 1970s. Unlike the prolonged stagflation of that era, current economic indicators and central bank policies suggest a resilience that makes a full-blown global recession driven solely by this bottleneck less probable, provided inflationary pressures remain managed.

The Global Oil Supply Chain and the Strait of Hormuz

Data presented below helps to identify how warranted or unwarranted investor reaction may be to the conflict in the Middle East. Separating the geopolitical risk premium from actual supply-demand fundamentals is crucial for long-term investors and their overall wealth planning strategies.

U.S. Oil Consumption vs. Domestic Production

The U.S. consumes about 7 billion barrels of oil per year, about the same as 20 years ago. Of this, approximately 50% is light sweet crude oil, 25% is medium crude oil, and 25% is heavy crude oil.

The U.S. produces about 4.8 billion barrels of oil per year. About three-quarters is light crude oil and the rest is mainly medium crude oil. Of the 2.2 to 2.5 billion barrels that the U.S. imports, it is mainly heavier oil. This is a counterpart to the types of refineries located in the U.S., many of which process heavier oil. Less than 10% of the U.S. oil imports pass through Hormuz. Most imports come from Canada. Here’s a breakdown of the global annual oil consumption:

- U.S. Consumption: 7 billion barrels

- World Consumption: 38-39 billion barrels

- Via Hormuz -Destination: 7 billion barrels (80%+ to Asia)

Global Oil Demand and Strategic Inventories

Worldwide oil consumption is about 39 billion barrels annually. About 7 billion passes through Hormuz, with about 6 billion headed for Asia (primarily China, India, and Japan). This represents about 35% of China’s demand for oil, and about 80-90% of Japan’s demand.

Global inventories total about 7 billion barrels. Surprisingly, less than 2 billion of this is strategic reserves controlled by governments. The rest are mainly reserves at the big companies (Exxon, Shell, BP etc.). Almost all 7 billion barrels of inventory are in friendly parts of the world. These inventories can help to keep up with demand.

The International Energy announced that it will release 400 million barrels of oil. The release of strategic inventories is designed to provide time to re-route tankers, increase production elsewhere, and reduce demand. The U.S., Europe, Russia, Canada, and Brazil are unlikely to see physical shortages. In contrast, Japan, South Korea, India, and China are heavily impacted. The oil market is global, so the U.S. still experiences spikes in prices. Markets will adapt to find alternative transportation routes to move the oil where it is needed. This includes complex supply chain realignments, such as diverting very large crude carriers (VLCCs) around the Cape of Good Hope, which adds transit time and freight costs, but ensures delivery or maximizing overland pipeline capacity where feasible. These logistical workarounds will serve as vital shock absorbers for the global energy market.

Other Commodity Disruptions To Pay Attention To

Beyond oil, a further wildcard is other commodities disrupted by the war: liquefied natural gas (LNG) from Qatar, urea for the manufacture of fertilizer, helium from Qatar (a critically important need for semiconductor production), and petroleum derivatives used in the production of plastics and chemicals, among others.

Conclusion: Navigating Short-Term Disruptions

This appears to be an oil disruption, which should be short-term in nature. Asia will see the worst of it. Oil supply will be rerouted and resourced through agile global supply chains. Even a small change in the market can make a big impact on oil prices. Likely to remain mostly an oil issue and less of an overall economic problem or a catalyst for a sustained recession.

Straight From Aufman Associates: Answering Your Top “Strait of Hormuz” Investment Questions

With sensational headlines warning of a 1970s-style energy crisis, how insulated is my portfolio against a severe, inflation-driven recession?

While daily market volatility can be unsettling, the current situation is primarily a logistical disruption rather than a fundamental economic crisis. Unlike the 1970s, the U.S. is highly insulated from Middle Eastern oil bottlenecks; we produce a massive amount domestically and import mostly from Canada, with less than 10% of our imports passing through the Strait of Hormuz. Because of our current macroeconomic resilience and proactive central bank policies, a full-blown, sustained global recession driven solely by this event remains highly unlikely.

The U.S. seems protected, but my portfolio includes international holdings. How will these oil bottlenecks impact investments with exposure to Asian markets?

It is true that Asia, specifically Japan, India, and China, will bear the brunt of the short-term impact, as a significant portion of their oil passes through the Strait of Hormuz. However, global markets are highly adaptable. We are already seeing the release of strategic reserves (such as the IEA’s 400 million barrels) and the rapid realignment of supply chains, including rerouting large tankers and maximizing pipeline capacities. These logistical workarounds act as vital shock absorbers, helping to stabilize global prices and mitigate severe, long-term damage to international equities.

The commentary mentions that investors are still finding opportunities in AI despite the rocky markets. Should we be shifting our strategy to lean more heavily into technology right now?

While it’s true that the underlying strength in technology sectors, especially AI, is providing a strong buffer against broader market panic, we do not recommend making reactionary, wholesale shifts based on geopolitical headlines. The current oil disruption is expected to be short-term.

The most effective approach is to maintain a disciplined, balanced investment strategy that captures the growth potential of AI while ensuring your overall wealth plan remains diversified and resilient enough to weather temporary geopolitical storms. See how we can help!